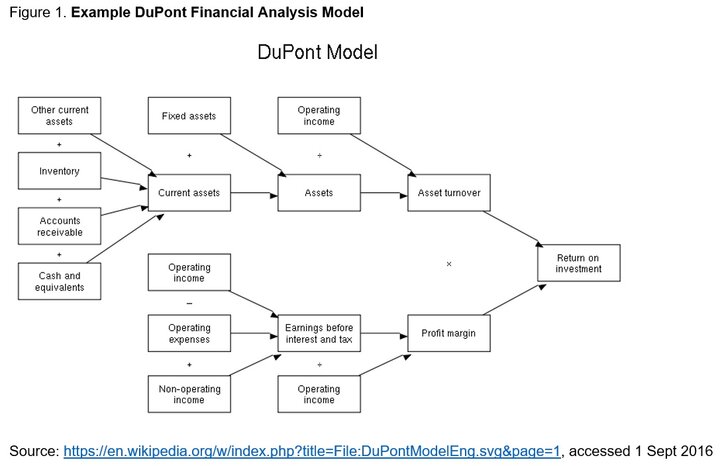

One challenge farm/ranch operators have is to accurately find where to make changes to an operation to increase profits. Many have the records and numbers but don’t know where to start. A system of financial analysis developed nearly 100 years ago by an explosive salesman for DuPont Explosives Company is a useful tool for farm/ranch managers analyzing financial performance. It is a simple system that can point managers in the right direction when looking for the correct places to make operational improvements. This avoids wasting time and effort chasing unicorns. The DuPont system relates the three factors of: 1) returns on investment, 2) earnings, 3) financial leverage and asset use efficiency and has a method to point to areas for improvement.

Let’s describe some of the math and explain how to use DuPont analysis (Figure 1). The final calculation is return on equity (ROE). ROE is calculated and then compared to a benchmark or desired return on equity. If ROE is lower than desired, first examine return on assets and compare it to a benchmark or desired return on assets (ROA).

If ROA is acceptable, then you know that the problem is with your financial structure. There may be too much short-term debt or higher than current interest rates. But if ROA is too low, the farm manager will look to the operating profit margin (OPM) and asset turnover ratio (ATR) to see if either or both are in line with benchmarks or expectations. If either is off, the farm manager can then follow back the calculations that make up that ratio. Thus the DuPont system of financial analysis allows a farm/ranch manager to follow a structured process to identify the cause or causes of lower than desired or needed financial performance.

There are possible disadvantages to using the DuPont system. Users must be certain that the benchmarks they use to compare with are calculated using the same asset valuation method as their own. The DuPont system uses ROE for its final calculation. Thus, the same method of asset valuations, cost or market, for the benchmark data set and the farm/ranch must be used for analysis to be valid. Otherwise a manager may be heading down the wrong path of the DuPont model when looking to make financial progress or may think the operation is doing well when it is not. Another possible problem with DuPont analysis is that the farm/ranch managers accounting documents are not very accurate and do not account for all sales, expenditures or assets. Again analysis will be incorrect when accounting documents are not accurate.

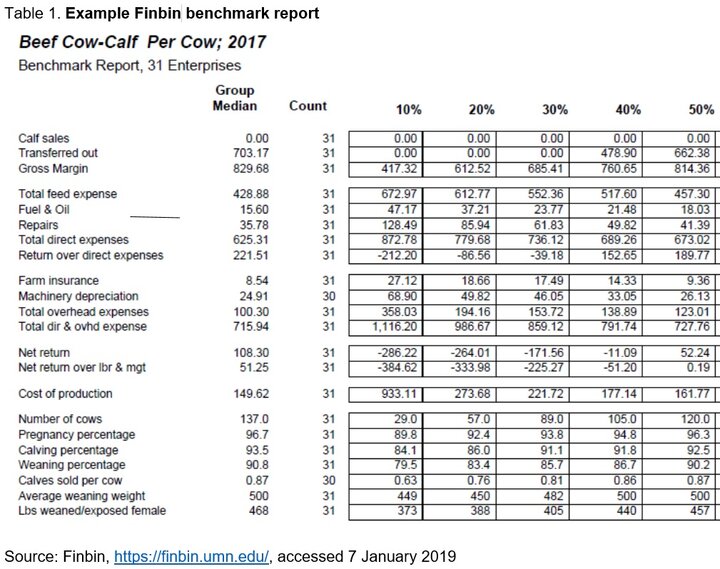

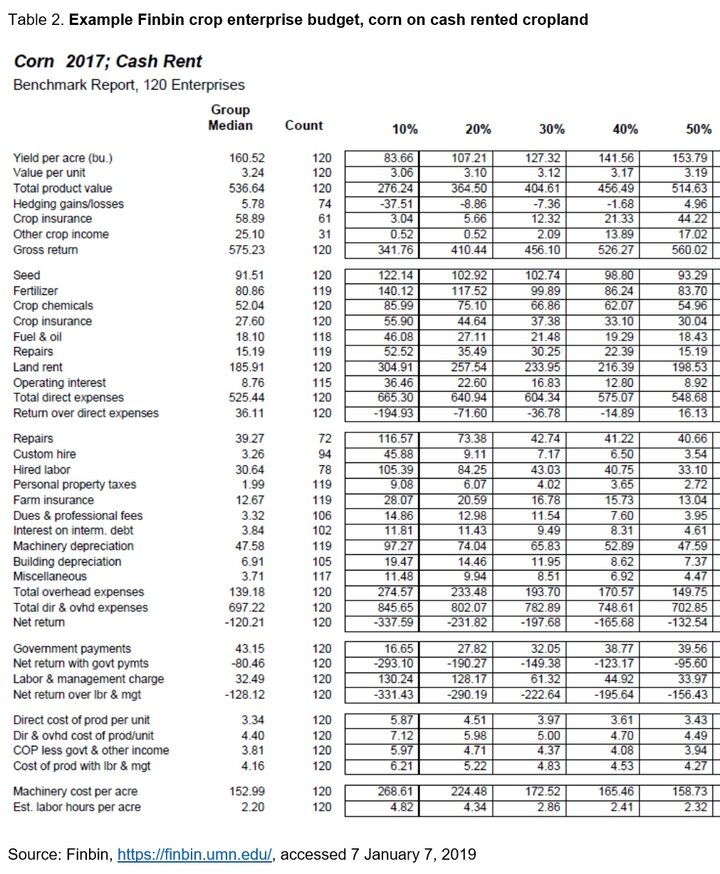

If the farm/ranch manager wishes to use the DuPont system finding a data set for benchmarking is necessary. One free and useful data set is Finbin. This data set is built from a large number of state farm business associations and is a farm level data set. Finbin has the ability to sort its data by crop enterprise, livestock enterprise and whole farm. This sorting can produce a report that is similar to Table 1. Table 1 only includes the first four profitability columns for readability; ten profitability columns are possible allowing a farm/ranch manager to compare their own profitability, liquidity and solvency measures to the columns and finding where their operation fits. Crop enterprise budgets are also available to use for farm/ranch benchmarking. These would be needed to compare when going back along the DuPont system flow chart to determine possible farm/ranch management changes. Table 2 is a crop enterprise budget, but there are livestock enterprises budgets available in the Finbin database. Also refer to the Nebraska Farm Business Inc. or Kansas Farm Management Association beef enterprise budgets for benchmarking data.

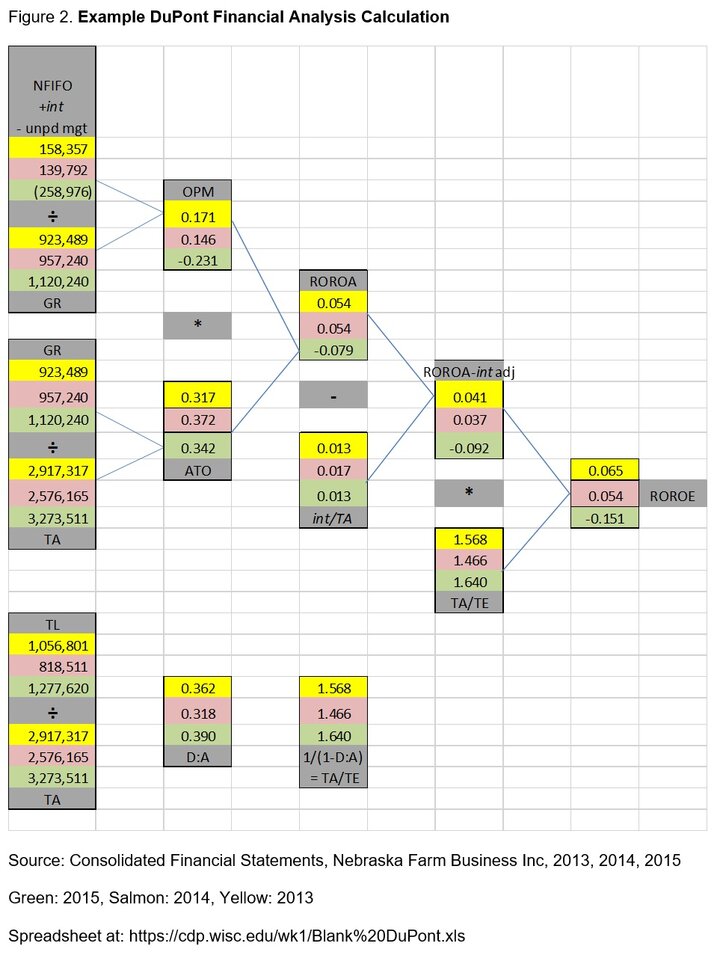

Here is an example (Figure 2) of how the DuPont model can be used to diagnose farm financial problems or ways to improve good results. This sample farm is a mixed operation where it runs a cow herd and has significant crop acres. It also operates a feeding operation buying feeders and selling at market weights. The numbers used to calculate the Figure 2 ratios came from the Nebraska Farm Business Inc. (NFBI) 2013-2015 annual reports at market valuations of assets.

The 2013 rate of return on equity (RORE) for our example was 6.5% while the average of all farms was 4.4%, for 2014 the RORE for our example was 5.4% and the average of all farms was 4.9%., for 2015 our example RORE was -15.1% while the average was -2.3%.

What happened to our sample farm? Following Figure 2 back along the negative ratios, we find Net Farm Income Farm Operations (NFIFO) was the culprit. Following the numbers back further, during 2013 the example operation had significant income from feeding. Then significantly more cattle were fed in 2015, compared to the year prior. Purchased feed was also much higher in 2015. Of the 2015 $258,976 NFIFO loss, just under $210,000 was due to the feeding operation. Now that we know where the biggest loss has occurred on the operation, we can use the benchmark data sets to find out the problems in feeding that caused the loss.

Looking at the past 3 years of operating profit margin (OPM) we can see why the farm operator may have taken a chance and bought many more feeder cattle in 2015 than past years. OPM is gross revenue divided by NFIFO adjusted for unpaid labor and interest costs. The OPM for the example farm 2013-2015 was 17.1, 14.6 and -23.1 respectively. The average OPM for the NFBI farms was 15.7, 17.9 and 20.9%. So our example had a big drop in gross net margin and decided to make up for that drop during 2015 by feeding more cattle with cheap corn.

The DuPont model along with benchmarks for agricultural enterprises can guide farm and ranch operators in their quest for higher profitability. The tools are adaptable to the records that farm and ranch operators already have.

Interviews with the authors of BeefWatch newsletter articles become available throughout the month of publication and are accessible at https://go.unl.edu/podcast.

Topics covered:

Budgets & cost of production, Marketing, budgets & management