Distillers’ grains play an important role in both maintaining ethanol plant profit margins and providing affordable, nutritious feed to livestock feeding operations. Distillers’ grains are produced as necessary by-products of the fuel ethanol production process and therefore rely on an input grain – most commonly corn in the United States – and fuel ethanol in their production (USDA ERS 2021). As a result, the primary tenets of the supply structure in the distillers’ grains market In the United States are fuel ethanol and corn, while livestock operations in need of feed products comprise the majority of distillers’ grain demand structure.

Ethanol plants sell these different types of distillers’ grains to livestock feeding operations since their high protein content accelerates weight gain and offers other favorable nutritional properties (Halfman 2020). While both MDGS and WDGS offer slightly higher feeding values than DDGS due to elevated digestibility from higher moisture contents, their moisture contents and weights make them difficult to ship beyond a limited radius (Nuttelman et al. 2011). As a result, WDGS and MDGS are purchased by producers generally within a 100-mile radius of an ethanol plant, whereas DDGS, the most common form of distillers’ grains nationally, can be shipped practically anywhere domestically or internationally (DeOliveira et al. 2017).

Each type of distillers’ grain offers desirable nutritional properties compared to corn due to lower starch content, higher total digestible nutrients, and higher crude protein content (Jenkins 2016). Thus, one tradeoff for livestock feeders is the relative price, on a dry matter basis, of distillers’ grains to corn on a dollar per ton ($/ton). Prices must be compared on a dry matter basis since corn, DDGS, MDGS, and WDGS all have different moisture levels and thus a different price base. One converts the price by dividing by one minus the moisture level. For example, DDGS is generally sold at a 10% moisture level. Assuming the price of DDGS is $300 per ton, the dry matter price is $333 per ton (i.e. 300/(1-0.10)).

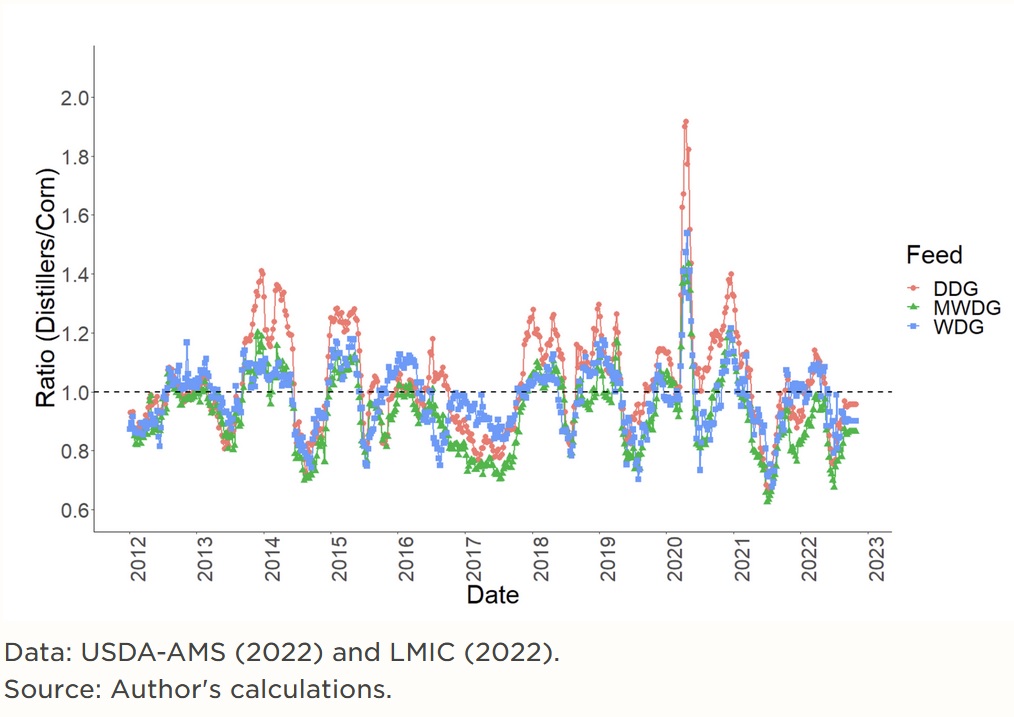

It has well known that agricultural markets were affected during the COVID-19 pandemic. The fuel ethanol and distillers grain market was no exception. The low corn stocks-to-use ratio and the ongoing Ukraine and Russia conflict have impacted the price of corn and thus potentially the price premium of distillers over corn from 2020 to the present. In this article, I assess the distiller grains market in Nebraska using weekly FOB bid level prices for DDG, MWDG, and WDG from ethanol plants reported by USDA Agricultural Marketing Service (USDA-AMS). Using this data from 2012-2022 I show how distiller grain prices in 2020-2022 compared to historical trends in the distillers to corn price ratio. The assumed moisture levels for the different feed products are 15% for corn, 10% for DDGS, 52.5% for MDGS, and 67.5% for WDGS.

Figure 1 plots the distiller’s grains to corn price ratio on a $/ton dry matter basis. Values greater than 1 indicate that distillers' grains are more expensive than corn. Values less than 1 indicate that the distiller's grain is cheaper than corn. The large spike in 2020 was when fuel ethanol plants shut down or idled due to the COVID-19 pandemic. We can also see that there are times before 2020 when distiller grains were more expensive relative to corn. This seasonal price pattern occurs in the third and fourth quarters as more livestock enter feeding operations during a time when fuel ethanol plants tend to be slowing production due to reduced demand for fuel ethanol. The combination of higher demand and reduced supply leads to relatively higher prices.

Another observation is that DDGS tends to be more expensive relative to MDGS and WDGS. Further, WDGS tends to be at or more expensive than MDGS. DDGS is relatively more expensive than the other distiller's grains because it has more potential buyers. It can be sold locally, shipped to other states, or exported. The ability to transport it longer distances increases the number of potential customers and thus increases the demand for the product. I believe that the premium of WDGS over MDGS is the effect of livestock feeders' preferences for feeding a wetter product in rations.

Table 1, panel (a) shows the probability of paying a premium for a distiller's grain and the average amount of premium ($/ton on a dry matter basis) one should expect in different years. Between 2012 and 2022, 52% of the time a producer would have paid a premium for DDGS over corn at an average premium price of $2.93 per ton. MDGS and WDGS were much lower at 30% and 45%, respectively. Both MDGS and WDGS have become relatively cheaper, on average, between 2020-2022 whereas DDGS has become more expensive.

Some producers have the flexibility of feeding different types of distillers in livestock rations and thus the relative difference between distillers is more important than the actual premium above corn. Table 1 panel (b) shows the probability of paying a premium and the average premium between different types of distillers. 96% of the weeks between 2012 and 2022 DDGS was priced more expensive than MDGS on a dry matter basis, 63% for DDGS-WDGS, and 25% for MDGS-WDGS for an average premium of $10.20 per ton, $5.16 per ton, and -$5.08 per ton. Since 2020, these price spreads have significantly widened.

Paying a premium for a distiller’s grain product does not necessarily affect the value proposition of feeding distillers grains in the ration. The University of Nebraska – Lincoln has conducted a large number of cattle feeding trials that compare diets with and without distillers’ grains at different inclusion levels (0-40% inclusion), with different base corn in the diet (dry rolled, high moisture, steam flaked), oil levels (full fat, de-oiled), and feeder cattle placement weights (calves, yearlings). The overall finding is that distillers still should be included in diets even at higher corn prices and price ratios, regardless of oil levels, because of the relative improvements in cattle feed efficiency. A summary of these findings is being published and will be available to the public sometime in January 2023. The conclusions of these trials are specific to feedlot cattle in Nebraska and may differ for cattle in the Southern Plains or for different livestock species (i.e. dairy cattle, hogs, and poultry).

| -- | Probability of Paying Premium (%) | Avg. Premium/Discount ($/ton) | ||||

|---|---|---|---|---|---|---|

| -- | 2012-2022 | 2012-2019 | 2020-2022 | 2012-2022 | 2012-2019 | 2020-2022 |

| Panel (a): Prices | ||||||

| DDGS | 52% | 52% | 56% | 2.93 | 2.15 | 5.12 |

| MDGS | 30% | 31% | 25% | (7.30) | (7.05) | (8.01) |

| WDGS | 45% | 48% | 36% | (2.23) | (2.24) | (2.20) |

| Panel (b): Price Spreads | ||||||

| DDGS-MDGS | 96% | 95% | 99% | 10.20 | 9.20 | 13.10 |

| DDGS-WDGS | 63% | 60% | 71% | 5.16 | 4.39 | 7.32 |

| MDGS-WDGS | 25% | 26% | 23% | (5.08) | (4.82) | (5.81) |

Source: Author's calculations

Note: Numbers in parathesis are negative numbers (i.e. (5.08) = -5.08)

Figure 1. Nebraska DDGS, MDGS, and WDGS as a Proportion of Corn Price on a Dry Matter Basis, 2012-2022.>

Interviews with the authors of BeefWatch newsletter articles become available throughout the month of publication and are accessible at https://go.unl.edu/podcast.

Topics covered:

Forage crop systems, Crop residues, Distillers feeds, Corn, Marketing, budgets & management, Marketing & risk management