This article was first published by In the Cattle Markets on Dec. 7, 2021

Cull cow prices have been considerably higher than in previous years. What has been most puzzling for producers is that prices have been rising in a period with increasing supply to the market. Common questions being asked are “Why are prices higher now than in previous years?”, “Will prices remain high into 2022?”, and “How do added costs due to higher feed prices impact overall profitability?”. Producers deciding to retain cows this winter to capture the elevated prices need to consider these questions before committing financial resources. So what do current fundamentals and historical cull cow prices tell us about future price trends?

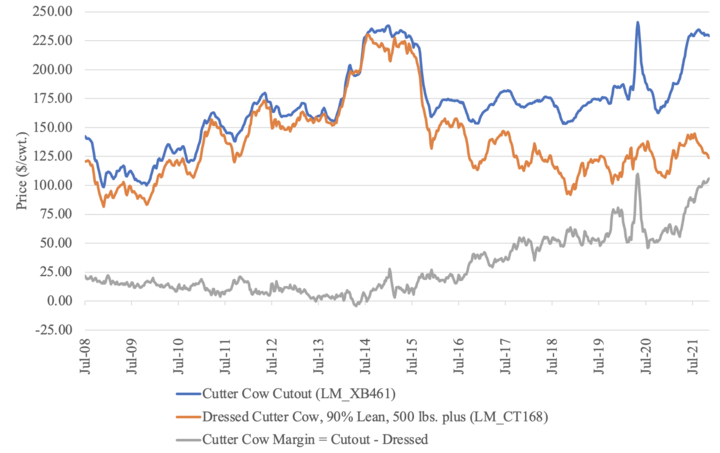

Overshadowing the rise in cull cow prices has been questions about competition and processing margins – which originated in the steer and heifer market and have now started to circulate in the cull cow market. One of the reasons is the increasing wedge between the wholesale cutout value for cull cows and the dressed price received by producers. Figure 1 plots these two price series and this margin from July 2008 to November 2021. Similar to what has been observed in the steer and heifer market, there has been a significant price deviation since the 2014-2015 time frame. What has been driving this wedge is still up for debate but it has led more producers to be curious about how the cutout is calculated and the drivers of seasonal patterns in the cutout. This justification is partially supported by the fact that cow-calf operations generally derive 10-20% of their income from selling cull cows.

Ground beef and merchandisable beef cuts are the market’s two primary purposes for cull cows. Ground beef comes from the U.S.’ unsatiable desire for hamburgers and other meals that include ground beef. Merchandisable beef cuts (i.e. tenderloin, ribs, etc.) from cull cows are primarily used in non-white tablecloth foodservice outlets that offer value steaks and other beef dishes. All the available supply into this market comes from 1) beef cows and bulls, 2) dairy cows, 3) trimmings and grind from steer and heifer slaughter, and 4) beef imports. These separate markets combine to impact the supply, and in part, the prices received, for cull cows. In the current year, we have seen an increase in beef cows and bulls harvested as the national cow herd contracts, an increase in dairy cow culling, volatile steer and heifer slaughter, and slightly higher beef and veal imports. All of these supply signals suggest higher supplies of ground beef to the market which should reduce price given a constant demand. However, demand for beef, ground beef in particular, has been historically strong. From this, we likely conclude that the rise in the wholesale and producer cull cow prices is being driven more by demand than supply signals.

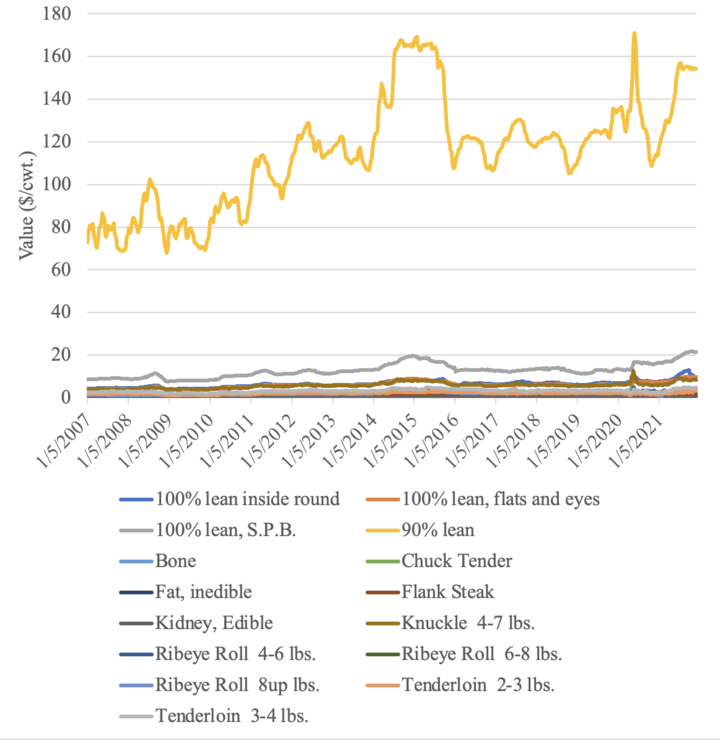

So how strong has the cull cow cutout been? It is important to note that the cutout is a calculated value determined by the composite share of value from different meat products. Figure 2 shows the weekly value of the 15 products that make up the cutter/lean cow cutout value from January 2007 to November 2021. Given that cutter/lean cows have a 45-49% dressing percent and 88-90% lean content, it is not surprising that most of the value is derived from 90% lean product and other lean meat products. Lean 90% beef accounts for approximately 70% of the value of the cutter cow cutout and this share has remained consistent over this time frame. The last time there was a similar run-up in 90% lean prices was during the 2014-2015 production year.

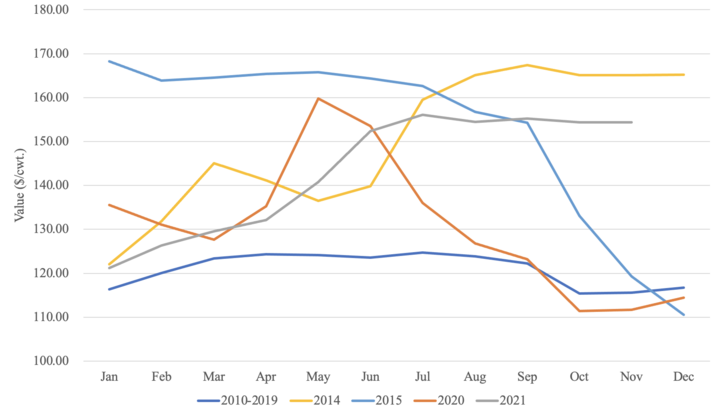

As with most commodities, there is seasonal price variation in the cull cow cutout. Prices for all quality cull cow grades (i.e. breaker, boner, cutter/lean, and canner/lights) tend to peak in the summer months – approximately in July – where there is still relatively strong demand for ground beef, strong demand for beef products in foodservice, and relatively lower supply of cull cows on the market. So why have the cutter cow cutout prices not seasonally declined as they should this fall? Figure 3 shows the seasonal price patterns for the value of 90% lean which consists of approximately 70% of the cutter cow cutout value. The last time this atypical seasonal pattern occurred was during the 2014-2015 production year. During that time frame prices stayed elevated for approximately 18 months until seasonally declining in the fall of 2015.

There are several reasons why the currently elevated cull cow prices may hold longer in the 2021-2022 production year compared to the 2014-2015 production year. First, in 2014-2015 the national cow herd was in a rebuilding phase implying that supply was contracting. Currently, the national cow herd is in a contraction phase and culling rates have been accelerated due to drought conditions. This implies more product is coming to the market now further reducing the future supply of cull cows. Second, feed prices were significantly lower in 2014-2015 compared to current feed prices. Cash corn was $3.79 per bu. and hay prices were $120 per ton. Compare these to current feed prices of $5.45 per bu. for corn and $145 per ton for hay. Higher feed prices create greater incentives to sell open, old, or nuisance cows rather than feeding to re-breed. Third, domestic beef demand is approximately 15% higher today than it was in 2014-2015. These, and other reasons, suggest that the atypical 90% lean beef patterns, and the cutout price in general, may persist into and beyond the 2022 production year. Ultimately, this implies continued elevated cull cow prices for producers across the different quality grades into 2022.

Topics covered:

Budgets & cost of production, Marketing & risk management, Marketing, budgets & management